Apr 15, 2026

The momentum in AI's two biggest names just flipped.

The flip from buy to sell interest for OpenAI in the secondary market is one of the sharpest I’ve seen in recent memory.

Over the past 12 months, we aggregated $4.5B of closed secondary transaction data and another $11B of buyer & seller interest. Our data produces signals, and the signals for OpenAI and Anthropic are diverging.

Here’s what we’ve seen on Caplight for OpenAI over the past year:

-- $520M in buy interest, which dried up in Q1.

-- $1B in sell interest, with Q1’26 being the most seller dominated quarter.

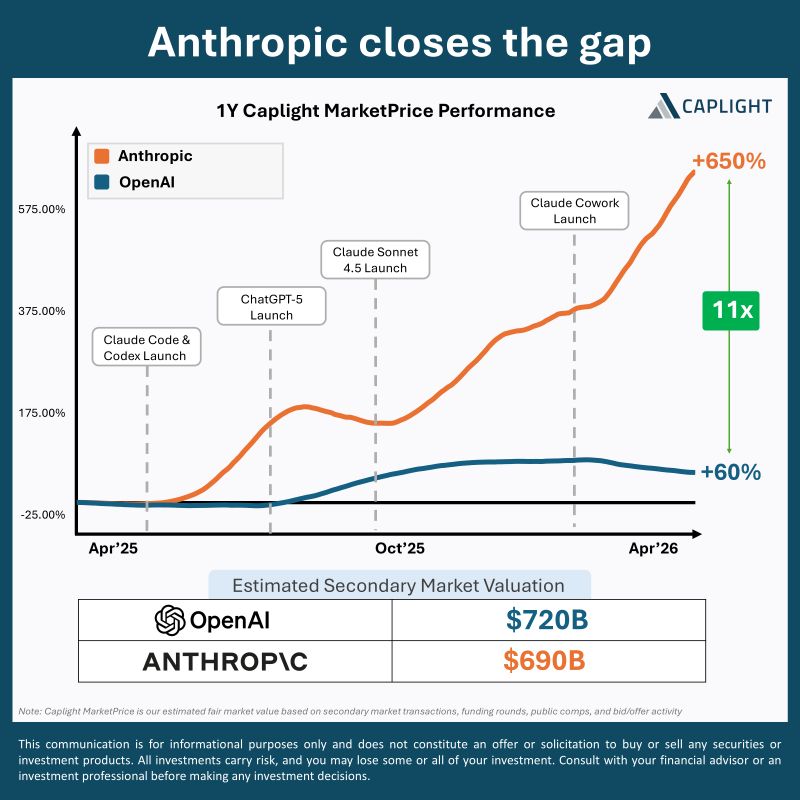

-- OpenAI MarketPrice is up +60% LTM, but down -10% over the last 3 months

And here’s Anthropic:

-- Buyers have flooded the market with $2B in buy interest.

-- $765M in sell interest, that was practically non-existent in Q1’26.

-- Anthropic MarketPrice is up +650% LTM.

In Q1 ‘26, OpenAI had 5x more sellers than buyers. One year ago, buyers dominated. Meanwhile, Anthropic had 6x more buyers than sellers, its highest ratio in the past year.

It’s hard to pinpoint a single event where this performance divergence began, it seems more based on the product cycle. Each major Anthropic release (Claude Code, Sonnet 4.5, Cowork) produced a sustained secondary market price increase. OpenAI's ChatGPT-5 and Codex, by contrast, generated brief upticks before fading.

To be clear, OpenAI is still the larger company by valuation. But momentum has shifted.

We estimate OpenAI’s current valuation based on observed secondary market transactions, and buyer/seller interest, at $720B, versus $690B for Anthropic.

If the IPO window does open this year, it’s going to be fun to watch which of these companies comes out at a higher valuation!

Disclaimer: This communication is for informational purposes only and does not constitute an offer or solicitation to buy or sell any securities or investment products. Consult with your financial advisor or an investment professional before making any investment decisions. Past performance is not indicative of future returns. Investments in private companies are illiquid, as there is a limited secondary market for private company shares.