Apr 23, 2026

VCs used to avoid the secondary market. Now they're almost half of it.

VCs used to avoid the secondary market. Now they're almost half of it.

A few years ago, a VC or fund selling on the secondary market was a red flag. Low quality. Distressed. A signal that something was wrong.

That stigma seems mostly gone.

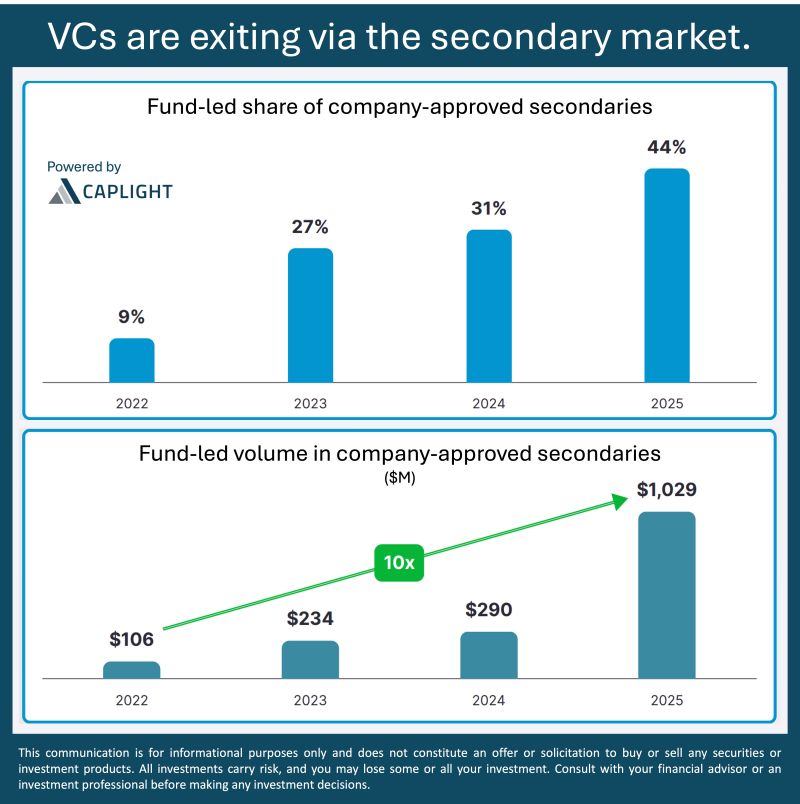

Three data points tell the story:

📈 44% of company-approved secondary volume in 2025 came from funds, up from 9% in 2022.

💰 That's $1B in fund-led volume, a 10x jump from 2022.

🏦 Two-thirds arrived in institutional-sized blocks ($10M+).

The signal is in the share class. Preferred shares typically sit with funds, not employees, so when preferred volume moves like this, it's portfolio management, not rank-and-file liquidity.

Caplight tracks transaction type and share class, which is how we isolate fund participation in the secondary market.

The why is simple:

- IPO window stayed narrow.

- LPs want liquidity.

- Secondary infrastructure matured: better data, more participants, no taboo.

What was once an employee-driven market is now being shaped by institutional capital flows. Funds stopped asking "should we sell on the secondary?" and started asking "how much, and at what price?"

Disclaimer: This communication is for informational purposes only and does not constitute an offer or solicitation to buy or sell any securities or investment products. Consult with your financial advisor or an investment professional before making any investment decisions. Past performance is not indicative of future returns. Investments in private companies are illiquid, as there is a limited secondary market for private company shares.